Overview of Business

Laurus Labs is a fully integrated pharmaceutical and biotechnology company, with a leadership position in generic Active Pharmaceutical Ingredients (APIs) and major focus on anti-retroviral, Hepatitis C, and oncology drugs.

Laurus Labs operate under four business units covering a wide range of therapeutic applications as mentioned below.

Laurus Generics - API - Development, manufacture and sale of APIs and advanced intermediates.

As per concall report Q3FY22, Overall demand declined due to inventory stocking at various channels, and management says that they are witnessing a normal trend from Q4 onwards.

Laurus Generics - Finished Dosage Form (FDF) - Company develops and manufactures oral solid formulations for low and middle-income countries (LMIC), North America and European Union (EU) markets. Backed by in-house API strengths.

As per concall report Q3FY22, The formulation division reported revenues of ₹ 1,389 crores for nine months with 13% growth. Whereas ₹ 373 crores for the quarter with a decline of 13%. The contribution from the formulation segment has improved during the nine months to 30% from 36% in the previous year.

Laurus Synthesis - Company provides Contract Research and Manufacturing Services (CRAMS) and Contract Development and Manufacturing Organization (CDMO) to global pharmaceutical companies and several late-stage projects. Steroids and hormone manufacturing capability.

Management says that, Concall Q3FY22, it was a very strong quarter for us and delivered robust growth of 63% year-on-year at INR 207 crores. For nine months FY ‘22 CDMO business also grew over 60%.

Laurus Bio - Recombinant products - animal origin free products for safer and viral free bio manufacturing.

As per concall report Q3FY22, this segment achieved a sale of INR 25 crores, taking to INR 65 crores from the nine months FY ‘22. During the quarter, Laurus Bio commissioned two more fermenters of 45KL each, taking the total capacity of 180KL.

The company also has a dedicated R&D team for developing processes and products to create a diverse range of medicines. Company has six manufacturing facilities and Laurus synthesis private limited in Visakhapatnam and a kilo lab facility in Hyderabad, which have received approvals from WHO, US FDA, PMDA, NIP Hungary, KFDA, ANVISA, JAZMP – Slovenia, EU (Germany), COFEPRIS and BfArM.

Revenue wise breakup as per Annual Report FY21.

I have my own frame of analysis which covers the following important analysis points as mentioned below.

Financial Analysis

Operating Efficiency Analysis

Margin of safety i.e. Self sustainability in the Business

Business Analysis

Size of opportunity

Fund flow analysis

Financial Analysis of Laurus Labs Limited

Let us analyze the financial performance of Laurus Labs Limited over the last 10 years. While analyzing the financial reports and available public documents of Laurus labs, it is very much clear that Laurus Labs has started to report consolidated financial reports from FY2014.

As we are trying to analyze the financial reports of Laurus Labs for the previous 10 years and hence we will analyze here the standalone financial reports for FY2012 and FY2013 and further we will analyze here the consolidated financial reports from FY2014 to FY2021.

Sales Growth

Over the last 10 years, the sales of the company have increased at a growth rate of about 30% from ₹451 Cr in FY2012 to ₹4814 Cr in FY2021. Further, the company reported higher sales too i.e. ₹4923 Cr in its last 4 quarters ending Dec-2021.

We must note here that if we see the standalone financial data, there is a slight decline in sales to ₹4728 Cr in its last 4 quarters ending Dec-2021 from ₹4769 Cr in FY2021.

While, if we analyze the trend in sales growth of the company, then we will notice here that the company has reported continuously higher sales year on year. There was never a decline in sales in the previous 10 years. Hence, we can say that the journey of the company over the last 10 years was very smooth in terms of sales.

₹719 Cr in FY13 from ₹451 Cr in FY12.

₹1160 Cr in FY14 from ₹719 Cr in FY13.

₹1778 Cr in FY16 from ₹1327 Cr in FY15.

₹2832 Cr in FY20 from ₹2292 Cr in FY19.

₹4814 Cr in FY21 from ₹2832 Cr in FY20.

I have tried to analyze the consolidated sales of the last 4 quarters ending Dec-2021 with the help of screener. Over the last 4 quarters ending Dec-2021, the sales of the company have decreased at a growth rate of - 7.61% from ₹1412 Cr in March-21 to ₹1029 Cr in Dec-21.

Reason for the decline in sales in the last 4 quarters ending Dec-21

While analyzing the reason for the decline in sales in the last 4 quarters ending Dec-21, I have tried to find out and noted below the reason with available resources such as concall.

Management says in its Q2FY22 concall that when it comes to generic API, our anti-retroviral business during the quarter was weaker than expected and declined 11% year-on-year to Rs.339 crores. Sequential drop is always due to continued demand stabilization in the channel as indicated in the last quarter itself. This is expected to stabilize in Q4.

Hence, Management is continuously pointing out the sequential decline in sales was basically due to decline in sales of generic API business. Decline in sales was basically due to continued demand stabilization in the channel.

Management is also pointing out in its Q2FY22 concall that In the generic API segment, other APIs predominantly consist of cardiovascular, diabetes and some asthma products, recording a 8% growth year-on-year and there is a decline of 20% in the first half of the FY '22. This decline has nothing to do with the business opportunities, it's only the scheduling of the delivery by CMO partners. So, scheduling of the delivery by CMO partener also contributed to the decline in sales of the generic API segment.

Management is mentioning in its Q3FY22 concall that the reason for lower sales and lower profit in Q3FY22 was basically due to lower sales in ARV API and formulation segments. Hence, demand has been less during the Q1, Q2, Q3 of FY22. Management is expecting that by Q4 it will be normal.

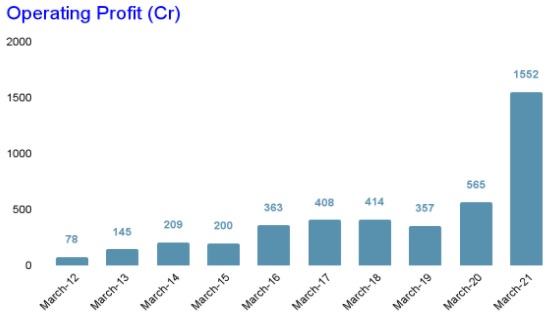

Operating profit and Operating profit margin

If we see the operating profit of the company in the last ten years, we will note here that the operating profit of the company has increased from ₹78 Cr in FY12 to ₹1552 Cr in FY21.

But, operating profit of the company in FY19 declined sharply to ₹357 Cr from ₹414 Cr in FY18. We will try to find out the reason for this sharp decline of ₹57 Cr. That reason will help us to have a sense of decline in operating profit in the coming future too if a similar situation repeats.

If we see the operating profit of the company for the last 4 quarters ending Dec-21, we will note here that like sales, operating profit of the company too declined to ₹285 Cr in Dec-21 from ₹472 Cr in March-21.

Reason for the drop in operating profit of the company in FY19

Let us see here what management says in its Annual report of FY19.

“The margins were affected due to the high raw material costs and incremental fixed operational expenses, pertaining to the new formulation facility. We expect formulation sales to increase with new approvals in regulated markets and enhanced traction in existing products and geographies. This will improve the margins for the Company as operating leverage will kick in.”

So it is very much clear that high raw material costs and incremental fixed operational expenses were the reason for reduction or declining in the operating profit and operating profit margin in FY19. These incremental fixed operating expenses were for a new formulation facility.

So whenever there will be an increase in raw material price, companies will face the similar problem of declining margins. It also indicates that the company does not have much pricing power in products in which it has significant market share as per FY19 financial report and annual report.

It is a very important point and we will keep this point in mind to understand further whether the company has secured the capability to pass on the incremental cost in raw materials to the customer or not.

The margins were affected due to the high raw material costs and incremental fixed operational expenses, pertaining to the new formulation facility. We expect formulation sales to increase with new approvals in regulated markets and enhanced traction in existing products and geographies. This will improve the margins for the Company as operating leverage will kick in.

Reason for the drop in operating profit of the company in last 4 quarters

Let us first see here what management is mentioning in its Q3FY22 concall about the drop in operating profit margin of the company.

“During the last quarter, our industry has faced some interim challenges due to logistics, raw material availability and higher prices, especially for solvents. Most of the solvent prices were at an all time high. We are seeing some -of these including the cost of API's and solvents and availability of raw materials. However, supply chain and logistics cost situations continue to remain challenging. ARV market saw continued sluggishness during the third quarter due to inventory at various channels. However, as we indicated before, we are expecting demand to increase from Q4 onwards.”

However management had mentioned in its Q2FY22 concall reports that they only buy solvents as raw material and further they develop the intermediate in house. These solvents cost between 5% to 10% (depending on the products) of the total raw material cost of the company.

“Right now, close to 50% of raw materials we buy from China and we don't buy any intermediates. All intermediates are made in-house. So, that way we are insulated from the fluctuations to a great extent. That's why our challenge is only to monitor the prices of solvent, which is a global phenomenon, not limited to the country, other than that because of our initiatives and also capacity creation for the backward integration, we are in a better question than people who import from intermediates and buy APIs from other countries”.

“The significant increase in price happened in the last week only. Some solvents went up by 10%, some solvents went up by 50%, some solvents went up by 200%, this varies, some solvents prices are normal, for example, ethanol prices were quite stable rather a little lower than what we anticipated, some solvents went up significantly”.

So, again the company is facing margin compression issues due to change in the raw material price. We have seen similar reasons in FY19 where the margin of the company was impacted due to increase in the raw material price. So, again the company is not able to protect its operating profit margin from increase in raw material prices.

But the good point is that the company is procuring solvent and they do not procure intermediate as they made intermediate inhouse.

Interest coverage ratio

While I prefer a company that has interest coverage of at least 3. If we see the interest coverage ratio of the company over the last 10 years, most of the times it was above our benchmark i.e. 3. There are only two instances, in last 10 years, where interest coverage ratio was dropped below our benchmark i.e. FY15 & FY19.

Interest outgo is continuously increasing year on year from ₹31 Cr in FY13 to ₹154 Cr in FY21 as debt is increasing year on year. The company is able to maintain its interest coverage ratio on a healthy side and even very much comfortably in FY21, because company operating profits have increased from ₹78 Cr in FY12 to ₹1552 Cr in FY21 with a CAGR of 39.42%. Therefore, we can think that the company would not find it difficult to service its debt even in tough times.

Debt to equity ratio

While I prefer a company that has a debt to equity ratio less than 1. If we see the debt to equity ratio of the company over the last 10 years, it has improved from 2.1 in FY2012 to 0.6 in FY2021.

Debt to equity ratio is not improved due to reducing the debt but also mainly it is improved due to increase in the equity of the company. Once, we will see the fund flow analysis, we will sense the use of funds coming from debt.

Operating Efficiency Analysis of Laurus Labs Limited

Net fixed asset turnover (NFAT)

Let us analyze the Net fixed asset turnover (NFAT) of the company in the last 10 years. We will notice here that Net fixed asset turnover of the company was continuously decreasing from 3.40 in FY13 to 1.47 in FY19. It again started to increase from FY20 and now as of FY21 it is 2.47.

While analyzing the reason for lower NFAT during FY16 to FY20, it was noted that the company was increasing its capacity. If we see the capex executed during these periods i.e. from FY16 to FY20, it is ₹1552 Cr.

Hence, Net fixed asset turnover (NFAT) of the company was lower because the company was executing capex and increasing the capacities but any new facility will definitely take time to generate the revenue.

Once new facilities started to generate the revenue, NFAT started to increase and as of FY21 it is 2.47.

Management is too saying that they have increased their capacity utilization during FY 2019-20 as per annual report of FY20.

Further while reading the Board's report in AR of FY20, it was noted that Formulation capacity utilization was at peak and management was planning for expansion of formulation capacity. All the units were operating at optimum capacity.

Therefore, NFAT of the company started to increase from FY20 as the company has now improved the utilization of its capacities.

Inventory turnover ratio

Let us analyze the inventory turnover ratio (ITR) of the company in the last 10 years. We will note here that most of the time the inventory turnover ratio (ITR) of the company was in the range of 3.3 to 3.9.

However, during FY13 and FY14, it was 5.6 and 4.8 respectively.

CARE has mentioned in its credit rating report of March-21, Laurus has a high inventory holding period as the company has to maintain buffer stock for validation of new products and R & D process apart from regular inventory requirement for production of drugs.

Analysis of receivable days

Let us analyze the receivable days of the company in the last 10 years. We will note here that receivable days of the company were always on a higher side and during FY18 and FY19, receivable days of the company crossed 100 too.

Cumulative cash flow from operation (CFO) vs Cumulative profit growth (PAT)

We can note here that cash flow from operation for the last 10 years is ₹2418 Cr and cumulative profit after tax for the last 10 years is ₹2100 Cr. So, we can note here that the company is able to convert its profits into cash flow from operation.

Here, over a period of last 10 years, cumulative cash flow from operation is higher than cumulative profit after tax. As we know that interest paid and depreciation will be deducted to determine PAT but will be added back to determine the CFO. Here, over the last 10 years, interest paid is ₹787 Cr and depreciation is ₹1010 Cr and it is an important factor that contributes to cumulative CFO being higher than the cumulative PAT.

Margin of safety in the business of Laurus Labs Limited

Self sustainable growth rate

The self sustainable growth rate of the company was continuously decreasing from FY15 to FY20. It was 17% in FY15 and continuously dropping to 0 in FY20. However, it suddenly jumped to 8% in FY21.

But if we see the sales growth of the company, we can note here that the company is growing at a much higher rate as compared with its self sustainable growth rate. In other words, we can say that the company was not able to grow with the pace as it was growing by using its own funds.

The company's self sustainable growth rate is much lower i.e. 8 % in FY2021 as compared with its sales growth which is 30 %. It indicates that the company will not be able to meet its growth plan with its internal resources, Hence, the company will have to be dependent on the outsource funds like debt and equity dilution.

In order to meet the growth rate requirement, the company was continuously taking debt year on year and we can see here that the company's total debt has increased from ₹225 Cr in FY2012 to ₹1482 Cr in FY2021 with debt growth rate of 23% during FY2012 to FY2021.

But, it is very good to see that company debt to equity is under control and as of FY2021 it is only 0.6 which is very good in my point of view. So, the company is taking debt but for growing its business year on year.

Dividend payout

During the period FY12 to FY21, The company has paid dividend ₹185 Cr and retained the earning by ₹1915 Cr.

Free cash flow

During the period of FY2012 to FY2021, the company has generated cash flow from operation ₹2418 Cr. During the same period, the company has executed CAPEX of 3306 Cr. So, if we determine here the free cash flow for the same period, it will be - ₹887 Cr.

Fund Flow Analysis

I have tried to summarize the flow of funds with the help of the following table. Fund coming to the company is indicated here in positive sign and fund going out from the company is indicated here in negative sign.

I have also given here the color codes for ease in understanding. Fund coming to the company is indicated here in green color and fund going out from the company is indicated here in red color.

Assumption : Let us focus here the major fund flow

So, let us see here from where the company is securing or generating the fund in FY2021

Company has secured ₹ 74 Cr from deferred tax - There was some deferred tax which has given an inflow fund of ₹ 74 Cr.

Company’s Equity has been increased by ₹ 831 Cr

Company has taken funds from borrowing (short term & long term) ₹ 360 Cr

Company has secured ₹ 83 Cr of funds in terms of other financial liabilities

During the current year ended March 31, 2021, the Company acquired 72.55% stake in Laurus Bio Private Limited {‘’Laurus Bio’’} (Formerly known as Richcore Lifesciences Private Limited) on January 20, 2021.

Laurus bio became the subsidiary w.e.f. January 20,2021. The Company further acquired 6.66% stake on February 10, 2021 from promoters of Laurus bio. As at March 31, 2021 the Company holds 79.21% stake in Laurus Bio Private Limited.

According to conditions stipulated in the Investment Agreement, the selling shareholders (Promoters) have “put option” over 20.79 % shareholding at any time between January 20, 2024 and January 20, 2026 for a consideration equal to their proportion of the equity value of Laurus Bio. As at March 31, 2021, this option has been recognized as a financial liability at the fair value of the redemption amount with a corresponding adjustment to other equity.

Trade Payable is ₹ 563 Cr. That means the company is using 563 Cr rupees from its creditors. This fund is also coming to the company in terms of trade payable.

Fund of ₹69 Cr and ₹37 Cr coming to the company in terms of Current maturities & other financial liabilities and other current liabilities respectively.

Therefore, the company is approximately securing a fund of ₹ 2017 Cr. I have left the small fund flow here which is less than ₹ 20 Cr for ease in understanding.

Now, let us see here how the company is utilizing this fund in FY2021

Company has utilized ₹ 503 Cr fund in procuring the assets like property, plant, equipment, taking equipment or assets on lease and CWIP which will be converted into fixed assets.

Company has purchased intangible assets of ₹ 237 Cr. I think this intangible asset is related to the acquisition of Richcore Lifesciences Private Limited.

Inventory piled up and ₹ 670 Cr of funds stuck here.

Fund stuck in trade receivable is of ₹ 515 Cr.

Cash and cash equivalent increased by ₹ 46 Cr

There are some prepayment and some balances with statutory/Government authorities, it is resulting a fund outflow of approximate ₹ 31 Cr

Therefore, the company is approximately utilizing or expending a fund of ₹ 2002 Cr. I have left the small fund outflow here for ease in understanding the major fund outflow.

Conclusion

So, now here, I am trying to make some sense that the company is utilizing the funds in purchasing assets, in acquisition of facilities like acquisition of Richcore Lifesciences Private Limited and raising the bank balance. These are the good utilization of funds.

It will be interesting to see here that there is some utilization of funds, like stucking of funds in trade receivable, inventories and balances with statutory/Government authorities, which is indicating the lack in operating efficiency of the company.

When we see the sources of funds, there is a major source of ₹ 831 Cr fund inflow to the company through equity and ₹ 563 Cr funds inflow in terms of trade payable. These sources of funds look good.

Funds are also coming to the company through borrowing of approximate ₹ 360 Cr. I think it is also not bad as the company is targeting to grow with 25 % to 30% in topline then the company has to arrange funds from outside like borrowing.

Business Analysis

Let us first find out the various key highlights in the business of Laurus Labs Limited during the FY20-21.

Completed acquisition of Richcore Lifesciences Pvt. Ltd, renamed as Laurus Bio, which is now a subsidiary of Laurus Labs.

Incorporated Laurus Ingredients Pvt. Ltd., a wholly owned step-down subsidiary of Laurus Synthesis Pvt. Ltd.

Completed four drug product validations, apart from the filing of 27 ANDAs and NDAs

Created additional formulation capacity by debottlenecking operations

Began construction of large formulation manufacturing block which will be available for commercial use starting Q3 2021

Started three new manufacturing blocks for commercial manufacturing of intermediates and APIs

Above highlights are for FY 2020-21, it indicates that Laurus Labs is focused on continuous growth.

Laurus has charted a definite growth trajectory that involves strengthening its presence in the non-ARV space, fortifying its position in the formulations and synthesis segments and tapping the new area of biologics (through Laurus Bio). The Company is looking to build new capacities/facilities that would propel its growth in the coming years.

Comparison of Laurus labs growth with its peers

Laurus Labs is showing outperformance with its peers in terms of sales and profit growth. Following table is self explanatory.

Size of opportunity

According to Grand View Research, the global pharmaceutical manufacturing market size was valued at US$ 324.42 billion in 2019 and is expected to grow at a compound annual growth rate (CAGR) of 13.74% from 2020-27.

Active Pharmaceutical Ingredients (API) industry

The global Active Pharmaceutical Ingredient market is expected to grow at a high single digit CAGR from 2020 to 2027 to reach US$ 364.17 billion by 2027.

Increased healthcare expenditure by the urban population and an increase in the geriatric population are influencing the market growth of APIs.

Let us see the opportunity for Laurus Labs in API space

The rising accessibility to affordable healthcare services has increased the demand for low-cost and high quality medicines, particularly in the developing world. Consequently, the need for low-cost and high-quality APIs are increasing for manufacturing finished drugs. Some of the key factors that are driving the market include the increasing prevalence of infectious diseases, cardiovascular conditions, and other chronic disorders.

Laurus currently supplies APIs to nine of the 10 largest generic pharmaceutical companies and has an advantage in backward integration. It also has a leadership position in APIs like antiretroviral drugs (ARVs), cardiovascular (CVS) and oncology. It is a major supplier for ARV APIs to other ARV manufacturers and finished drugs in several LMIC markets.

Generics market

According to Precedence Research, the generic drugs market size is projected to be worth around US$ 675.20 billion by the end of 2030. The global generic drugs market is expected to grow at a CAGR of 5.7% over 2021-30; the market is valued at US$ 387.92 billion in 2020.

In 2020, North America commanded a market share of more than 30%, with the US being the highest shareholding country in the region, mainly due to its advanced healthcare infrastructure, increasing occurrence of chronic diseases, and presence of leading players in the region.

The Asia-Pacific generics market had total revenue of US$ 129.90 billion in 2019, China accounted for 53.7% of the value of the Asia-Pacific market, followed by Japan and India with 21.1% and 12.7%, respectively. The China generic drugs industry market is anticipated to continue dominating the market in terms of revenue share.

Let us see the opportunity for Laurus Labs in the Generics market

Laurus has filed 27 Abbreviated New Drug Applications (ANDAs) with United States Food and Drug Administration (FDA) and has nine final approvals and eight tentative approvals. In addition, completed four products validation at commercial scale.

Antiretroviral (ARV) market

Antiretroviral therapy (ART) is a crucial step in reducing HIV-related deaths. The year 2020 was already a significant year with regard to HIV before the COVID-19 pandemic swept across the globe.

There was a sharp drop in HIV testing and viral load volumes as clients avoided clinics. In a survey conducted by the World Health Organization (WHO) in June 2020, 38 countries reported disruption in HIV testing services (HTS). ARV supply chains and HIV prevention outreach were disrupted due to lockdowns across the globe.

According to the Clinton Health Access Initiative – HIV Market Report, the number of patients (re-) initiating ART continues to increase, with over two million adult patients added between 2018 and 2019. In GA Low Medium Income Countries (LMICs), adult ART coverage increased from 64% in 2018 to 70% in 2019.

Let us see the opportunity for Laurus Labs in the Generics market

Being the cost leader in many ARV APIs, Laurus is best placed to garner attractive market share in ARV APIs and the Finished Dosage Form (FDF) tender market. The ARV portfolio consists of ~12 APIs, covering both 1st line and 2nd line treatment regimens.

Large-scale, improved manufacturing processes have been the key factors in making Laurus the preferred API supplier in the ARV segment. At present, Laurus is supplying 80% of the players who participate in ARV tenders. Being a fully integrated player, Laurus has a natural advantage and a superior margin profile compared to non-integrated players.

CRAMS industry

The global market for Contract Research and Manufacturing Services (CRAMS) is expected to grow at 7% CAGR in 2019-25 on the back of increasing costs of R&D, coupled with significant revenue loss due to impending patent cliff that has forced major pharmaceutical companies worldwide to outsource part of their research and manufacturing activities to low-cost countries like India.

CRAMS is one of the fastest-growing sectors in the pharmaceutical and biotechnology industry. The pharmaceutical market uses outsourcing services from providers in the form of contract research organizations (CROs) and contract manufacturing organizations (CMOs).

India offers significant cost advantages over matured manufacturing hubs in Europe and North America and has already emerged as one of the leading cost-competitive and quality manufacturing hubs for many global players including big pharma companies. The domestic CRAMS market is expected to reach US$ 40 billion by 2030.

Let us see the opportunity for Laurus Labs in the CRAMS industry

Laurus is uniquely positioned to address customer needs at any stage of the product life cycle. With over 150 scientists to provide process chemistry services to global clients, our contract development and manufacturing organization (CDMO) division is well positioned to offer development and manufacturing services across the value chain from preclinical to lifecycle management. Laurus has created a wholly-owned subsidiary – Laurus Synthesis Pvt Ltd – to increase its focus and dedicated R&D.

Nutraceutical industry

According to Mordor Intelligence, the global nutraceutical ingredients market size is projected to reach US$ 167.30 million by 2026, from US$ 127 million in 2019, at a CAGR of 4.0% during 2021-26.

Due to the increasing frequency of lifestyle diseases consumers across the globe are becoming health conscious. There is also a growing geriatric population with their own health preferences and conditions.

In consequence, consumer choice is shifting from chemically-derived products to protective healthcare items such as nutraceuticals that contain safer, natural and healthier ingredients.

Health consciousness, leading to healthy eating habits and consumption of nutrient rich food is increasing the adoption of fortified foods. These growing choices are expected to drive the growth of the nutraceutical market size. A positive outlook towards medical nutrition owing to increasing weight management programmes, along with the management of cardiovascular diseases, is anticipated to propel the demand for nutraceuticals.

Let us see the opportunity for Laurus Labs in the Nutraceutical industry

Laurus Labs has been at the forefront of the development and manufacture of pure, well-characterized specialty ingredients in the nutraceutical/dietary supplements and cosmeceutical segments. Its key strength lies in the development of alternative low-cost synthetic routes for naturally derived nutraceutical products. Patented combinations of nutraceuticals and pharmaceuticals may create rewarding business opportunities, going forward.

Overview of Indian Pharma Industry

The Indian pharma industry is poised for a big leap forward in this decade. Health, science and innovation have come into sharp focus as never before. The developments over the past year have emphasized the importance of an innovation ecosystem, a robust infrastructure for production of drugs and pharmaceuticals and the need to constantly build a huge talent pool of scientists, researchers and technologists who can be the arrowheads for the future.

India has emerged as a pharmacy to the world, supplying critical drugs and vaccines in the course of this pandemic. As per the report on the Indian Pharmaceutical Industry 2021 by FICCI and EY, during 2020-30, Indian pharma industry is expected to grow at a CAGR of ~12% to reach US$ 130 billion by 2030 from US$ 41.7 billion in 2020.

Strength in the business

CARE Rating has compiled, in its credit report of March-21, the strength and weakness in the Laurus Labs business very beautifully. Let us see some strength and weakness points from CARE Rating credit report.

Healthy Growth

During FY20, the company at consolidated level has achieved around 23.5% growth in its total operating income which stood at Rs.2,836.59 crore during FY20. The total operating income of the company improved on account of foray into formulations segment on large scale and healthy growth in synthesis and other API segments. The growth in the revenue is primarily attributable to Finished Dosages Form segments which increased to Rs.825.3 crore in FY20 from Rs.54.6 crore in FY19. The other segment which contributed to the growth in the topline is the Synthesis segment which increased by 30.71% to Rs.385.1 crore in FY20 from Rs.294.6 crore in FY19.

The PBILDT margin has improved from 15.74% during FY19 to 20.10% during FY20. The profitability has increased due to change in composition of revenue from API to formulations, i.e., 75.25% and 2.38% during FY19 to 49.82% and 29.15% during FY20, respectively.

Completion of strategic acquisition to augment growth in turnover

Laurus, as per its press release date February 10, 2021, has acquired a majority stake (74.37%) in Richcore Life Sciences Private Limited (Richcore). The cost of acquisition of 74.37% was Rs.260.24 crore and was funded through internal accruals.

Richcore is a research-driven biology company having fermentation capabilities and ability in animal origin free recombinant products. These products help vaccine, insulin, stem cell-based regenerative medicine and other biopharma customers, eliminate dependency on animal and human blood derived products and in turn produce safer medicines.

Laurus through this acquisition is projecting to penetrate into established enzyme segments, vaccines and become a dominant player in CDMO space in Mid- Term. Apart from this, Laurus had also acquired bulk drug manufacturing unit from Phalanx Labs Private Limited, located at Visakhapatnam, Andhra Pradesh on a slump sale basis and it would be reflected in its subsidiary, Laurus Synthesis Private Limited (LSPL) which is incorporated in May 2020.

Growth opportunities in Formulations and Synthesis division

During FY20, Laurus commenced its formulations segment from unit 2 on a large scale which has the capacity of manufacturing 5 billion tablets per year. The formulations segment typically has higher asset turnover and better margins as compared to the generic API business which is reflected in the current year profitability. The company is targeting both developed markets (USA, Europe and Canada) and emerging markets (Global fund tenders, WHO Tender, PEPFAR Tender, and various African In-Country Tenders).

The company has cumulatively filed 26 ANDAs, 2 Para IV and 7 FTFs for North America and filed 9 dossiers in EU markets, 12 dossiers in Canada. During FY20, Laurus has launched 6 new FDF products under various therapeutic segments and are targeted to be supplied primarily to Low Middle Income Countries (LMIC) like Kenya, Tanzania, Malawi, etc. Laurus is focusing on synthesis division and revenue contribution has been increasing from this segment year on year for the last 4 years.

Strong product portfolio catering to therapeutic segments like ARV and Oncology

Laurus has a portfolio with more than 60 commercialized APIs with strong presence in ARV, Oncology, anti-diabetic and Hepatitis C therapeutic segments. Furthermore, the company has forayed into formulation on a large scale from Unit II in FY20 resulting in major revenue being contributed from that segment, i.e., about 29% in FY20 as against about 2% during FY19.

During February 2019, the company received approval for few of its products which caters to ARV segment and consequently the commercial sales took place during FY20.

Reputed and geographically diversified customer base with strong flow of repeat business mitigating revenue concentration risk

The top 10 clients of the company accounted for 62.05% of the total revenue in FY20 against 65.73% during FY19 reducing the risk of revenue concentration from clients y-o-y. Laurus added new customers in the Low Middle Income Countries market due to significant developments in formulations segment during FY20.

Existing customers in anti-retroviral and oncology such as Mylan Laboratories Ltd, Aurobindo Pharma Ltd and Natco Pharma Limited continue to contribute to significant revenue. During the year, the revenue from the domestic market has declined from 53% in FY19 to 35% in FY20. The decline is due to lower offtake of Efavirenz in South Africa eventually resulting in lesser requirements from domestic players who in turn supply to African markets.

Further, the revenue from the export market has increased from 47% during FY19 to 65% during FY20. Major portion of export sales is streamed from Africa and European markets. Exports to Japan, China and USA have increased in FY20 compared with FY19. Exports to Africa and USA are primarily finished dosages and exports to other parts of the world primarily constitute APIs.

Weakness in the business of Laurus Labs

Moderate operating cycle:

Laurus has moderate operating cycle period which has improved to 146 days during FY20 as against 161 days during FY19. The improvement in operating cycle is attributable to reduction in collection period from 110 days to 104 days in FY20 and increase in creditor days from 68 to 88 days in FY20. The inventory holding period was 130 days in FY20 as against 120 days in FY19.

Laurus has a high inventory holding period as the company has to maintain buffer stock for validation of new products and R & D process apart from regular inventory requirement for production of drugs. Average utilization of fund-based limits including CP (Rs.200 crore outstanding as on June 22, 2020) for the past 12 months ending December 2020 stood moderate at 63.99%.

Foreign exchange fluctuation risk

Laurus is exposed to foreign exchange fluctuation risk in view of large volume and high value transactions of export and import, a phenomenon common to the players in the industry.

However, for Laurus, the risk is mitigated to a certain extent as the contracts have clauses embedded for the exchange rate fluctuation and there is natural hedging through netting off the imports and exports to a large extent.

Exposure to regulatory risk

The company is exposed to regulatory risk as the pharmaceutical industry is highly regulated in many other countries and requires various approvals, licenses, registrations and permissions for business activities. The approval process for a new product registration is complex, lengthy and expensive.

I hope you have enjoyed the complete fundamental analysis. Please share to reach up to max people.

Thanks to my Mentors Ishmohit Sir, Anand Gurjeev Sir and Dr Vijay Malik Sir.

No comments:

Post a Comment