Deepak Nitrite Ltd

I will analyze today, for educational purposes only, Deepak Nitrite Ltd. I will break down the fundamental analysis in the following sections as mentioned below.

About the company - what does the company do?

Product portfolio and applications areas

Major areas of business

Sources of earnings - Segmental revenue

Financial Highlights : Trends of Sales, Operating profit, PBT and Net Profit over the years

Financial Highlights : Trends in Sales, Operating profit and Price to earning

Financial Highlights : Trends in Gross profit margin, EBITDA Margin, Net profit margin, ROIC, ROCE, ROE and EPS

Strength in the company

Weakness in the company

Conclusion

Deepak Nitrite Limited - what does the company do?

Since 1972, Deepak Nitrite has been a leading intermediates company in the Indian chemical industry to serve the domestic and international market with high quality products made in a responsible and sustainable manner.

Product portfolio and applications areas

It's very important to study the products of a company and its application areas. Product portfolio will let us know about the various products offered by the company and we can figure out the raw materials required for producing it.

We can also figure out about the costing of raw materials and various factors affecting the costing of its raw materials. The Cost of raw materials affects the company operating profit and hence its very important to keep close monitoring over the price of raw materials used in a business.

For example, Deepak Nitrite raw materials are very much linked with the price of crude oil. Because most of the raw materials used at Deepak nitrite are developed from crude oil.

Deepak nitrite management also mentioned in their conference call about the linkage of raw material prices with price of crude oil.

Deepak Nitrite is in manufacturing of following products. We will study about these products in detail in this article ahead.

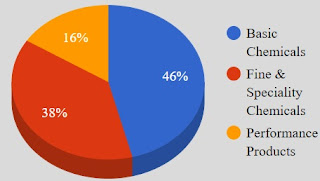

- Basic Chemicals

- Fine & Specialty Chemicals

- Performance Products

Following chart indicates the segmental revenue of Deepak Nitrite

Applications areas

It's also necessary to understand the application areas of the products offered by the company that we are studying as slowdown in end user industries will surely affect the performance of the company.

While studying and tracking any company or any business, we need to observe and note various data e.g. cost of raw materials, factors affecting the costing of raw materials, end user industries growth rate etc.

So, let us see here where Deepak Nitrite products are getting used.

Size of opportunity

We must understand the size of opportunity of a business in the coming years to ensure the growth of business in coming years. If the size of opportunity is large, it indicates that the company will have a strong opportunity to maintain its growth rate ahead.

The Indian chemical industry is one of the fastest-growing in the world. It encompasses over 80,000 commercial products, is widely diversified, and can be categorized into bulk chemicals, specialty chemicals, agrochemicals, petrochemicals, polymers, and fertilizers.

India is the world’s 6th largest producer of chemicals and contributes 3% to the global chemical industry. It is the 3rd largest producer in Asia. It is also the world’s 3rd largest consumer of polymers and 4th largest producer of agrochemicals.

The Indian chemical industry was valued at US$ 178 billion in CY2019 and is expected to grow at a 9.3% CAGR to US$ 304 billion by CY2025. In India, specialty chemicals account for 22% of the total chemicals and petrochemicals market.

Looking ahead, for the period FY 2020-25, demand for chemical products is anticipated to improve at a rate of about 9% annually. This will be led by demand for specialty chemicals and supported by demand for petrochemicals and polymers.

Therefore, Indian chemical companies have raised their capital expenditure commitments substantially in the past couple of years. Capacity expansion will be undertaken across the domestic industry and this is expected to translate into strong business performance.

By CY2025, the Indian chemical industry will have contributed around US$ 300 billion to

the country’s GDP, aiding India’s journey towards a US$ 5 trillion economy. The agrochemicals market is expected to grow at an annual rate of 8%, reaching US$ 3.7 billion in FY 2021-22 and US$ 4.7 billion in FY 2024-25.

Moreover, the chemical industry has been amongst the least affected by pandemic-related lockdowns, owing to its significance across the key end-user industries, including pharmaceuticals.

As a result, it is anticipated to outperform the country’s GDP growth, going forward. The

Government of India identifies the chemical industry as an important growth driver; it is

expected to account for 25% of the manufacturing sector’s GDP by CY2025. In fact, India’s per capita chemical consumption is low compared to other developed countries, making India a desirable investment and growth destination.

The growth of the chemical industry in India can be attributed to the following pillars of progress:

Establishing an alternative sourcing destination : China +1

Over the past two decades, there has been overdependence on China as the key source for several building blocks in the global supply chain. While there has been awareness among global customers of the competence of Indian players, based on parameters such as quality, costs, consistency, and environment management, the shift in market share up to the last decade was gradual.

This structural imbalance was sharply exposed during the pandemic, and now leading global players are seeking alternative sources for raw materials and intermediates in an accelerated manner, presenting strong prospects for Indian chemical majors to leverage this opportunity.

Enhanced focus on R&D:

The Indian chemical industry has been expanding its R&D footprint. As it strives to enhance its global market share, leading players are deploying strategies that

offer more than just cost competitiveness.

In order to increase wallet share, the focus has shifted to value addition, and this has

sharpened the focus on R&D. The drive is now to develop products in an innovative manner in order to emerge as a global hub for specialty chemicals.

Improved infrastructure:

There has been a prioritization of infrastructure development in India in recent years. Apart from improvement in ports, airports, highways, inland waterways, storage infrastructure, and logistics, the drive to establish focused industrial parks and zones is accelerating the development of local industry.

Setting up of PCPIRs (Petroleum, Chemicals, and Petrochemicals Investment Regions) with single-window clearances and improved all-round facilities is beneficial for the Indian chemical industry.

Growth rate of chemical industries in India

The chemical industry in India has come of age and has been able to further elevate its position in the global marketplace since the outbreak of the COVID-19 pandemic.

Despite the significant growth in recent years, it is fair to say that its potential is only beginning to be revealed. The growth drivers are in place and the coming years and decades will reap the benefits.

Major areas of business : Analysis of Deepak Nitrite’s products

Let us deep dive in to products offered by Deepak Nitrite

Basic Chemicals (BCC)

Sodium Nitrite

Sodium Nitrate

Nitro Toluidines

Fuel Additives

Nitrosyl Sulphuric Acid

Basic chemicals are utilized in colorants, Petrochemicals, rubber industries, Explosives, Dyes, Pigments, Food colors, Pharmaceuticals, Petrol & diesel blending and Agrochemicals.

Basic chemicals segment reported revenues of Rs. 516 crore in H1 FY22 as against Rs. 319 crore in H1 FY21, higher by 62%. Despite constraints around logistics and input cost pressures, the Company prioritized strategic opportunities to pass on increased costs while maintaining growth in market share. The performance was also supported by a favorable demand scenario augmented by shift towards India by global customers due to supply chain challenges.

Fine & Specialty Chemicals:

DNL manufactures niche and specialized products under its Fine & Speciality Chemicals segment (FSC). These are developed inhouse, using the Company’s expertise in process engineering and technical knowhow.

Among other things, it produces specialty chemicals such as Xylidines, Oximes, and Cumidines. These products are specially tailored to the client’s specifications and are typically manufactured in lower volumes, but command higher value.

In the FSC segment, revenues stood at Rs. 405 crore in H1 FY22 as compared to Rs. 350 crore in H1 FY21, a growth of 16%. Moving ahead, the Company is strategically tying up more business in multiyear formula kind of contracts with quarterly pass through mechanisms to insulate from the volatility in RM prices. In a significant development, the Company entered into a medium term contract with one of the world’s leading agrochemical majors, which will result in business sustainability.

The Fine & Speciality Chemicals segment (FSC) is utilized in Agrochemicals, Colorants, Pigment, Pharmaceuticals and personal wellness.

Performance Products (PP)

The performance products (PP) segment of the Company has two key products at present: Optical Brightening Agents (OBA) and DASDA. These products have specific attributes and serve to enable particular characteristics to the end-product.

DNL is differentiated as a fully integrated manufacturer of OBA, with operations commencing from conversion of basic input toluene into PNT and thereafter into DASDA and further into OBA. These products must meet stringent performance criteria and technical specifications as specified by global clients. Given its expertise and technical knowhow, DNL has been able to establish itself as a preferred supplier and has also strategically diversified its clientele across geographies and end-user industries.

The performance products (PP) segment is utilized in Paper, Detergents and Textiles.

In the PP segment, revenues grew by 55% to Rs.198 crore in H1 FY22 vs. Rs. 128 crore in H1 FY21.

Following chart indicates the segmental revenue of Deepak Nitrite.

Trends of Sales, Operating profit, PBT and Net Profit over the years

Figures in Rs. Crores

Sales of the company have grown from 1327.16 Cr in FY2015 to 4359.75 Cr in FY2021. Sales have grown each year except for a minor decline in FY2017 as displayed above.

Operating profit of the company has grown from 140.34 Cr in FY2015 to 1252.02 Cr in FY2021. Operating profit of the company has grown each year except for a slight decline in FY2017 as displayed above.

Net profit of the company has grown from 52.90 Cr in FY2015 to 775.81 Cr in FY2021.

Trends in Sales, Operating profit and Price to earning

Let us see here sales growth, Operating profit margin and Price to earning ratio with the help of the following table.

After looking at the trends of above mentioned parameters with the help of the following table, we can say that a company is able to protect its profitability over the years as margins are either increasing or maintained over the years.

Trends in expenses as percentage of sales

Trends in expenses as percentage of sales provides the information about the expenses where the company is using its earnings from sales over the years. It will also give information about various key information like where a company is saving money over the years and where the company is increasing its expenditure over the years.

Strength in the company

Long operating history and established track record in the global chemical intermediates industry

DNL has been operating in the chemical industry for nearly five decades. Over the years, the company has grown to become a market leader in the domestic market for inorganic intermediates (sodium nitrite and sodium nitrate), nitrotoluenes and fuel additives. It is also among the top three global players for xylidines, cumidines and oximes.

Diversified product profile mitigating risk associated with cyclicality in different product segments

While the company started with a limited portfolio of low-value bulk chemicals, it has grown its product portfolio to include high-value specialty chemicals for multiple end-user applications. Currently, it has a product portfolio of over 100 products (including its derivatives).

The company has also added pharma intermediaries and more agro-chemical products to its portfolio over the years. The regular introduction of new products has helped DNL to mitigate the cyclicality risk related to a particular product segment.

Multi-purpose manufacturing facility, with significant backward and forward integration linkages

The company’s production facilities include processes that allow vertical integration for most products, leading to significant cost savings. Also, its facilities are designed to provide flexibility to change the product mix to suit market requirements.

Healthy improvement in financial profile

DNL reported a significant growth in revenue and operating profitability over the years as studied above. With healthy cash accruals, the company has reduced its debt levels and as a result, the Total Debt/EBITDA improved to 0.47 times in FY2021 from 3.88 times in FY2019.

Healthy ramp-up of phenolics and IPA operations at DPL

DPL’s phenol-acetone plant showcased over 100% capacity utilization in 9M FY2021 in spite of the plant shutdown during April 2020 due to the Covid-19 pandemic, resulting in healthy revenue and cash flow generation for DNL on a consolidated basis.

DPL also commissioned an IPA plant in April 2020 and its utilization reached 85% during 9M FY2021. IPA is extensively used as a sanitizer, and with the Covid-19 pandemic, the global demand for IPA peaked in Q1 FY2021. With timely commissioning, DPL has been able to sell its product in the domestic and global markets, while generating healthy cash flows.

Weakness in the company

Profitability exposed to volatility in raw material prices, although reduced in certain products through formula-linked price contracts

Prices of a few of the company’s key products are linked to the movement of crude oil prices. The change in price levels, however, varies across product categories and is not equivalent with the change in crude price due to formula-linked pricing.

Also, the prices of certain key products, such as sodium nitrite, TFMAP, OBA and DASDA, which formed about 40% and 43% of DNL’s standalone sales in FY2020 in 9M FY2021, respectively, are delinked from movement in crude oil prices.

Capacity expansion and efficiency improvement capex planned over near term

While DNL had sizable capex plans for FY2021, it has deferred part of the same to next year, given the Covid-19 uncertainties. The company now has a planned capex of ~Rs. 950-1,000 crore to be incurred over FY2022-FY2023 towards expansion projects in the BC and FNS segments and addition of downstream products in the phenolics segment.

Such sizable capex plans expose the company to execution and market risks, although mitigated to some extent by the track record of the company in completing its past projects, including the phenol-acetone project under DPL, in a successful manner.

months. Further, DNL has an additional sanctioned loan facility of Rs. 150 crore from Axis Bank, which can be availed for any capex if the need arises. The loan terms are favorable, with an 18-month moratorium period from disbursement and a 10-year ballooning repayment schedule.

Conclusion

DNL, as part of a strong chemical industry, has a vital role to play in India’s move towards becoming a US$ 5 trillion economy and then to further benefit from that growth.

Despite the pandemic hurdles in the short to medium term, the Company is in a business that can only grow in the long term, especially with policy focus on general manufacturing, agricultural, and pharmaceuticals.

The domestic market of India is huge and has tremendous potential to grow; alongside, the Company has an established presence in international markets, too. This is an advantageous spread that helps the Company identify opportunities anywhere as soon as they begin to emerge.

The Company has the agility, product portfolio, manufacturing excellence, and sustainability focus to seize opportunities arising in any of the geographies where it is present or may enter in future, as its operations are aligned with the latest norms. Its speciality solutions offer precision and optimal efficacy to customers who demand international standards.

As global companies look to diversify sourcing, the China+1 focus is set to be a major growth driver for the Company.

Phenol is contributing to the concept of a self-reliant India, as the Phenol and Acetone segment clocked record turnover and solid margins. The wholly-owned subsidiary showed extreme resilience during the pandemic in ensuring material movement, and plant capacity utilization was consistently outstanding.

During the most difficult times, DPL commissioned its IPA plant and met the domestic demand for sanitizers; IPA capacity is now being doubled to 60,000 MTPA. This performance has proved the Company’s capabilities, and the main aim of this business vertical would remain import substitution (for IPA products from China, Korea, and Taiwan) and introduction of more value-added products.

Note :

This Post is only and only made for educational purposes and hence this post should never be considered as a recommendation.

Reference

Annual Reports, Concalls and credit rating reports.

No comments:

Post a Comment