Gufic BioSciences Ltd

I will analyze today, for educational purposes only, Gufic Biosciences Limited. I will break down the fundamental analysis in the following sections as mentioned below.

About the company - what does the company do?

Journey over the years

Major areas of business

Sources of earnings - Segmental revenue

Strength in the company

Financial Highlights : Balance Sheet and Other parameters

EBITDA and EBITDA Margin over the years

Gross Profit and Gross Profit Margin over the years

EBIT and EBIT Margin over the years

Net Profit Margin over the years

Bargaining power of the buyers

Bargaining power of the suppliers

Manufacturing Facilities and capacities

Investment Thesis

Antithesis - Risk analysis

Company overview

Gufic Biosciences Limited operates in a single segment i.e., Pharmaceutical. The pharmaceutical industry is one of the world's fastest growing industries and among the biggest contributors to the world economy.

Gufic Biosciences Ltd is a fast-growing pharmaceutical player recognized for its innovative, high-quality pharmaceutical and herbal products and a wide range of APIs (Active Pharmaceutical Ingredients).

Gufic is engaged in the research and development, manufacturing, marketing, distribution and sale of pharmaceutical and allied products. Gufic is known and respected for innovative and high quality pharmaceutical and herbal products along with a wide range of Active Pharmaceutical Ingredients (APIs).

Gufic is one of the fastest growing companies among the top 100 pharma companies in India and is also one of the largest manufacturers of Lyophilized injections in India and has a fully automated lyophilization plant.

Gufic lyophilized products are available in Therapy areas like Antibiotic, Antifungal, Cardiac, Infertility, Antiviral and proton-pump inhibitor (PPI).

Gufic is now augmenting its global focus by deepening its presence in the priority markets of India, Germany, Switzerland, South Africa, Russia, Canada, Europe and other key countries within the emerging market territories.

Gufic aims at providing lifesaving drugs to people at affordable prices with no compromise in its quality.

Gufic Biosciences Limited is a WHO-GMP, EU GMP, ANVISA Brazil, Russian GMP, Health Canada, Ukraine GMP, Australia TGA, Colombia INVIMA and Uganda NDA approved company with a total capacity of 30 million lyophilized vials per annum.

Gufic offers a varied therapeutic basket in its Bulk drugs / API division. The categories of API's manufactured are Antifungals, Antibacterials, Anesthetics and Intermediates for Antifungals.

Gufic's products are widely circulated across 1,500+ hospital chains and have leading medical facilities through an extensive network of 1000+ Field Force across India.

Journey over the years

Following figure is displayed here to show how Gufic has been shaped up over the years.

Major areas of business

There are three basic areas, as mentioned below, of business Gufic has.

Branded Domestic Business

Having created leadership brands in the anti-infective lyophilisation injectable categories, it is now expanding into other areas like Derma, Orthopaedic and Gynaecology –backed again by lyophilisation and R&D expertise to create differentiated product offerings.

CMO – Domestic, International Business

In the year 2007, Gufic Initiated contract manufacturing of lyophilized products. Gufic offers 170+ lyophilized products across multiple therapy areas. Gufic is a valued and trusted CMO partner, serving more than 70 companies in India. One of the largest suppliers of Doxycycline, Tigecycline, Gonadotropins, Liposomal Lyo Amphotericin B, Micafungin.

API Business

API business is the third business category of Gufic. Special facility is dedicated to API. Strategically important due to backward integration helping de-risk import dependence. The categories of API’s manufactured are Antifungals, Antibacterial, Anesthetics and Intermediates for Antifungals.

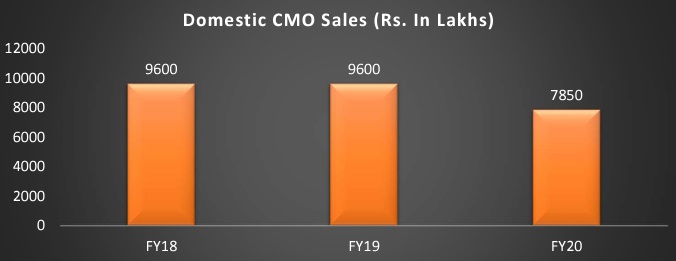

Sources of earnings

The product portfolio of the company is well diversified, marked by its presence in key therapeutic segments (under bulk drugs/API division) such as antifungal, anti-bacterial, anti-infective, anti-inflammatory, and anesthetic.

GBL’s lyophilization product includes antibiotic, antifungal, cardiac, infertility, antiviral, and proton pump inhibitor segments. The product portfolio can be divided mainly under two segments which includes pharma and bulk drugs. Pharma segment includes manufacturing and trading of Tablets, capsules, ointment, syrup/suspension powder, injection and lotion etc.

Following chart indicates the business wise sales mix.

Strength in the company

Vast experience of the promoters in the pharmaceutical industry

The promoters of the company have been in the pharmaceutical industry since 1960, through incorporation of Gufic Pharma Private Limited (GPPL). Gufic group has been in the business of manufacturing and marketing injectable products since late 1970s. The promoters are supported by qualified professionals heading various verticals with adequate and relevant experience in their respective fields.

Reputed and broad clientele base

GBL has long-standing relationships with its customers which include large players like Glenmark Pharmaceuticals Ltd, Lupin Ltd, Abbott Healthcare Pvt Ltd and Zydus Healthcare Ltd etc. Healthy relationships with reputed pharma players has led to repeat orders contributing to revenue growth over the years. Besides, it has a network of 25 carrying & forwarding agents and more than 500 stockists PAN India through which it has access to more than 1 lakh retailers. The top 10 customers contribute 30-35% to the revenues. GBL will continue to benefit from its well-established customer base.

Comfortable financial profile:

GBL has large capex plans which are to be funded through internal accruals and as a result despite huge capex, financial risk profile is expected to remain strong over the medium term.

Borrowings reduced from 27.55% in March-12 to 15.70% in March-21 as a percentage of total liabilities and it is also a good point.

Financial Highlights

Let us see here some financial numbers of Gufic Biosciences Limited.

Balance Sheet

If we observe the balance sheet of Gufic Biosciences Limited, we will find out that reserves increased from 15.89% in March-12 to 41.76% in March-21 and it is a good point.

Borrowings reduced from 27.55% in March-12 to 15.70% in March-21 and it is also a good point.

EBITDA and EBITDA Margin

Following chart indicates EBITDA and EBITDA Margin from March-12 to March-21. Chart is self explanatory.

Gross Profit and Gross Profit Margin

Following chart indicates Gross Profit and Gross Profit Margin from March-12 to March-21. Chart is self explanatory.

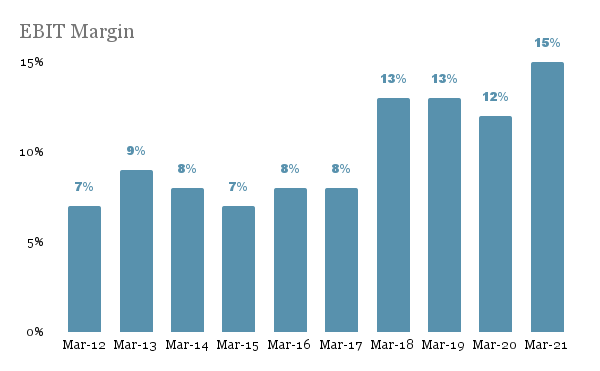

EBIT and EBIT Margin

Following chart indicates EBIT and EBIT Margin from March-12 to March-21. Chart is self explanatory.

Net Profit Margin

Following chart indicates Net Profit Margin from March-12 to March-21. Chart is self explanatory.

Bargaining power of the buyers

Let us check here the margin stability of the company from March-12 to March-21. Data studied above indicates that the company is maintaining its operating profit margin or EBIT margin over a period of time and it indicates that the company has good bargaining power over its buyers or customers.

Bargaining power of the suppliers

Let us check here the gross margin stability of the company from March-12 to March-21. Gross margin data indicates that the company is maintaining its gross profit margin over a period of time and it indicates that the company has good bargaining power over its suppliers too.

Manufacturing Facilities and capacities

Navsari Plant

Lyophilized Formulation, API and Herbal Manufacturing Facility

Lyophilizer –14.4 Million vials per annum

Ampoule –12 mn p.a.

Ointment –6 mn tubes p.a.

Lotion –6 mn bottles p.a.

Syrup –6 mn bottles p.a.

Baroda Plant

Sanitary napkins –0.7 mn per day

Belgaum Plant

60 mn capsules p.a.

3.6 mn powder p.a.

Investment Thesis

Is the market opportunity huge enough to provide a long runway to growth?

The global pharmaceutical industry

The global pharmaceutical industry has seen an increased use of medicines over the past decade where the rate of growth of medicine usage has outpaced both population and economic growth.

This expansion has been largely on account of the pharma emerging markets. As per Global Medicines & Usage Trends to 2025 report by IQVIA in April 2021, the global pharmaceutical market, estimated at US$1.27 Trillion in 2020, is expected to expand at a Compounded Annual Growth Rate (CAGR) of 3-6% to US$ 1.5-1.6 Trillion by 2024 and the growth excludes further spending on COVID-19 vaccines and the total cumulative spending on COVID-19 vaccines through 2025 is projected to be $157 billion, largely focused on the initial wave of vaccinations to be completed 2022.

It is anticipated that the key constituents of the global pharmaceutical industry shall remain with the USA owing to its size and with pharma emerging markets due to their growth prospects.

The growth in this market is predicted on the basis of various factors like market drivers, current and upcoming trends, current growth pattern, and market challenges. This growth is fueled by the growing and aging population in key markets.

As per World Population Prospects by the United Nations, the worldwide population is likely to cross 9.3 billion by 2050 and around 21% of this population is expected to be aged 60 and above.

Apart from aging and rising population the improvements in purchasing power and access to quality healthcare and pharmaceuticals to poor and middle-class families worldwide also is driving the growth of the global pharmaceutical industry.

Another aspect which is leading this growth is the rising focus of pharmaceutical companies to tap the rare and speciality diseases market. Innovations in advanced biologics, nucleic acid therapeutics, cell therapies and bioelectronics & implantable have attracted investments in the industry by even non-pharma companies like Facebook, Qualcomm etc. which is also driving the global pharmaceuticals industry growth.

It is expected that there will be newer treatment options available for rare diseases and cancer in developed countries, though they may come at a higher cost to patients in some countries, whereas in pharma emerging markets, wider access to treatment options and increased spending on medicines will have a positive impact on health outcomes.

Pharmaceutical spending in the developed markets grew at ~4% CAGR between 2014-19 and is estimated to grow at about 2- 5% CAGR to reach US$ 985-1015 Billion by 2024. These markets accounted for ~66% of global pharmaceutical spending in 2019, and are expected to account for ~63% of global spending by 2024.

Indian Pharma Industry – an overview

India is the largest provider of generic drugs globally. The Indian pharmaceutical sector supplies over 50% of global demand for various vaccines, 40% of generic demand in the US and 25% of all medicine in the UK.

India is a prominent and rapidly growing presence in the global pharmaceuticals industry. It is the largest provider of generic medicines globally, occupying a 20% share in global supply by volume, and also supplies 62% of global demand for vaccines.

India ranks 3rd worldwide for production by volume and 14th by value. India has the highest number of US-FDA compliant Pharma plants outside of the USA, and is home to more than 3,000 pharma companies with a strong network of over 10,500 manufacturing facilities.

India enjoys an important position in the global pharmaceuticals sector. The country also has a large pool of scientists and engineers with a potential to steer the industry ahead to greater heights. Presently, over 80% of the antiretroviral drugs used globally to combat AIDS (Acquired Immune Deficiency Syndrome) are supplied by Indian pharmaceutical firms.

Indian drugs are exported to more than 200 countries in the world, with the US being the key market. It is expected to expand even further in the coming years. The Indian pharmaceutical exports, including bulk drugs, intermediates, drug formulations, biologicals, Ayush & herbal products and surgical, reached US$ 24.44 billion in FY21.

Indian Pharma Market (IPM) was valued at US $ 24.0 Billion in MAT June 2021, the market showed a growth of 14% on an annualized basis, whereas the monthly growth was 12%. Top 7 therapies of IPM contributed 67% to the total sales. Respiratory Therapy posted the highest growth of 23% over last year and other major therapies like Anti-Infectives, Vaccines and Immunomodulators continued to show high growths.

According to the Indian Economic Survey 2021, the domestic market is expected to grow 3x in the next decade. India's domestic pharmaceutical market is estimated at US$ 42 billion in 2021 and likely to reach US$ 65 billion by 2024 and further expand to reach ~US$ 120-130 billion by 2030.

Indian pharmaceutical companies' sales are expected to grow robustly in the financial year ending March 2022 (FY22) as sales normalize in categories affected by the pandemic in the previous year. Most Indian pharma companies reported resilient operating performance in the financial year 2020-21, benefitting from gradual stabilization after the first quarter of financial year 2021-22, geographical diversification and sales of pandemic-related drugs. Sales of drugs used to treat acute medical conditions and elective procedures continue to recover in the financial year 2021-22.

Sales in these categories fell in the financial year 2020-21 as travel restrictions reduced doctor visits and hospitals prioritized Covid-19 treatment over elective procedures. The risk of further waves of infection remains significant in markets with slow roll-outs of vaccination, including India, but healthcare systems are better prepared after the second wave, which should limit the impact.

So, after looking over global and Indian pharmaceutical industries, we can say yes there is a huge opportunity to provide a long runway to growth.

Is company capable to capture the market opportunity

The total revenue increased to Rs. 49,143.16 lakhs in the financial year 2020-21 against the total revenue of Rs. 38,462.76 Lakhs in the previous year 2019-20, thus registering a growth of about 27.77% and net profit after tax increased to Rs. 4423.17 lakhs from Rs. 2268.80 lakhs, in previous year, a percentage increase of 94.96%.

During the FY21, the Company majorly concentrated on its domestic business focusing on the needs of people to overcome COVID-19 and hence, the total revenue of the Company for the year constituted to around 87.78% of its business consisting of domestic branded business sales, contract manufacturing and the sale of Active Pharmaceutical Ingredients and the balance 12.22% to exports business.

Gufic continues to strengthen product portfolio through new launches, many of them being first-to market products, offering significant patient benefits.

Apart from new launches, many of Gufic's existing products continue to grow their market share. The Company from April 01, 2019 till the date of this report have launched about 8 new products in the market, which also boosted the sales of the Company.

Due to the launch of new products, improvisation was made to the existing products and providing medicine at affordable prices to the consumer without compromising on the quality of the product.

The growth of the Company can also be evidenced from the MAT ranking progression of the Company as per IQVIA, which is as below

Gufic believes a diversified product basket helps to grow the business consistently and continuously. Gufic has identified complex and differentiated products in multiple therapeutic areas from where it will launch the next phase of growth.

Gufic's strategy of developing the specialty business as an additional growth engine has started delivering, with a gradual ramp up in specialty revenues. It is expected this momentum to continue over the next few years although the COVID-19 pandemic and lockdowns may throw up some uncertainties in the near-term. Gufic will continue its investment in Research and Development in spite of the current economic scenario.

Gufic has initiated Trials for D-29 has for the novel second-generation lipoglycopeptide antibiotic that belongs to the same class as vancomycin, the most widely used and one of the few treatments available to patients infected with methicillin-resistant Staphylococcus aureus (MRSA)and the launch of the product is expected by February, 2022.

Gufic drug candidate O-26 for the treatment of community-acquired bacterial pneumonia and acute skin and skin structure infections will be ready for commercialization by the end of the financial year 2022-23.

Gufic is also working on gynecology products and is currently working on three new molecules in the gynecology segment and is expected to be ready for commercialization by second quarter of 2021-22.

Apart from new first to launch molecules, Gufic also plans to launch new drug delivery systems in the field of Antibacterial and also Biological peptides by 2021 and DCGI process will be initiated by December 2020 with infrastructure tie ups from Spain and Italy.

So, yes, the company is capable of capturing the market opportunity.

Is shareholder major beneficiary of the growth in business:

We have already studied above the margin stability of the company from March-12 to March-21. Data studied above indicates that the company is maintaining its operating profit margin or EBIT margin and gross margin too over a period of time and it indicates that the company has good bargaining power over its buyers and suppliers too.

Company is having good pricing power as the company is able to maintain its margin over the years.

Look over the ROIC and ROCE. It indicates that the company is continuously generating profit over the years.

Look over the cash flow from operation activities for 2020 and 2021, it is 47 and 89 Cr respectively. But when you will see the net cash flow it is 0.36 Cr and 1.94 cr respectively. After analyzing the cash flow statement, it is observed that the business is generating cash from its core activities and the company is using this cash to purchase the fixed assets and in repaying the borrowings.

Borrowings reduced from 27.55% in March-12 to 15.70% in March-21 as a percentage of total liabilities and it is also a good point.

So the company is basically preparing its base and using its cash to expand its capacity. We have also studied above that GBL has large capex plans which are to be funded through internal accruals and as a result despite huge capex, financial risk profile is expected to remain strong over the medium term.

If we look over the compounded sales growth, compounded profit growth and stock price CAGR, we can say that business is growing fast and the company is continuously paying dividends to its shareholders.

Valuation

I am putting here some valuation ratio which could help to make a sense of the valuation of the business currently.

Antithesis - Risk analysis

Conclusion

Business is consistently growing over the years, business is having capabilities to maintain its margins and profitability. This report should be used for education purposes only and there is no buy or sell recommendation.

No comments:

Post a Comment